Equities

Piero Cingari

·

May 28, 2025

·

Benzinga

Piero Cingari

·

May 28, 2025

·

Benzinga

After a sharp Tuesday rally fueled by optimism over improved U.S.-EU trade ties, Wall Street stalled midweek as rising Treasury yields reasserted pressure ahead of Nvidia Corp. (NASDAQ:NVDA)’s earnings report and the release of key Federal Reserve minutes.

Major U.S. stock indexes paused on Wednesday, digesting recent gains as yields on longer-term Treasury bonds resumed their climb. The S&P 500 slipped 0.2% to 5,900 points by midday in New York, while the tech-heavy Nasdaq 100 held flat. Small-cap stocks underperformed sharply, with the Russell 2000 down 0.8%.

Sector performance was broadly negative, with 9 of the 11 S&P 500 sectors trading lower. Technology and communication services were the only sectors managing to avoid losses.

All eyes are on Nvidia, which is set to report earnings after Wednesday's closing bell. Wall Street expects earnings per share of 88 cents and revenue of $43.2 billion, according to Benzinga Pro estimates.

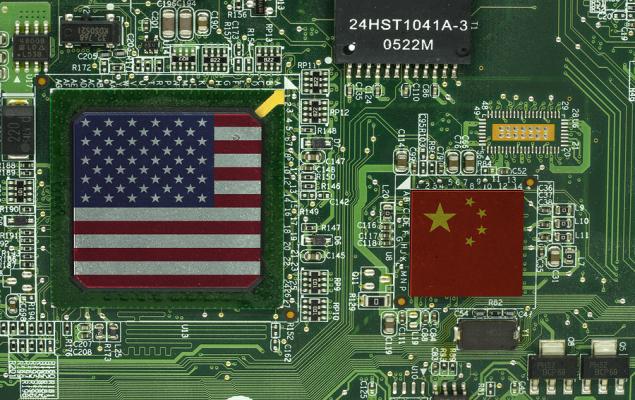

Beyond the headline figures, investors will be closely watching two key aspects: the impact of the U.S. export ban on the H20 chips destined for China and the forward guidance. CEO Jensen Huang already said the company could face a $5 billion annual earnings hit due to export restrictions, making this quarter’s outlook pivotal for market sentiment.

The Federal Reserve's minutes from its May meeting will also be released. The Federal Open Market Committee left rates unchanged in the 4.25%-4.50% range. Chair Jerome Powell signaled little urgency to cut rates, citing inflation risks partly tied to newly proposed trade tariffs.

Markets will parse the minutes for hints on the Fed's timeline for easing monetary policy, particularly as inflation data remains stubbornly elevated.

After a brief relief, bond markets came under renewed pressure. The yield on the 30-year Treasury note climbed 5 basis points to 5%, while the 10-year yield rose to 4.5%. Investors remain concerned about the trajectory of U.S. fiscal policy, with swelling budget deficits raising doubts about long-term debt sustainability.

The U.S. dollar rallied for a second straight session, decoupling from other U.S. assets. Meanwhile, gold slipped 0.2%, dipping below $3,300 per ounce. Bitcoin (CRYPTO: BTC) fell 2%, trading near $107,000 as speculative appetite in cryptocurrencies waned.

| Major Indices | Price | 1-day % |

| Nasdaq 100 | 21,427.45 | 0.0% |

| S&P 500 | 5,908.48 | -0.2% |

| Dow Jones | 42,230.96 | -0.3% |

| Russell 2000 | 2,074.61 | -0.8% |

According to Benzinga Pro data:

Stocks reacting to earnings reports include:

Stocks slated to report earnings after the close include Nvidia Corp, Agilent Technologies Inc. (NYSE:A), Synopsys Inc. (NASDAQ:SNPS), HP Inc. (NYSE:HPQ), Salesforce Inc. (NYSE:CRM), Nordson Corporation (NASDAQ:NDSN), e.l.f. Beauty Inc. (NYSE:ELF), nCino Inc. (NASDAQ:NCNO), C3.ai Inc. (NYSE:AI), Veeva Systems Inc. (NYSE:VEEV), Pure Storage Inc. (NYSE:PSTG), and SentinelOne Inc. (NYSE:S).

Now Read:

Image: Shutterstock

August 1, 2025

·

Benzinga

Copyright © Traders & Quants